Strengthening Singapore’s Social Security System

Singapore’s Social Security System has revolved around our CPF schemes, ever since CPF was introduced in 1955. After a good 65 years, 2021 will be a year of major upgrades, with all 3 insurance schemes under the CPF going for some enhancements, namely the Dependent Protection Scheme (DPS), MediShield Life, and CareShield Life. Here, we detail some of the changes that will be taking place progressively from March 2021.

Dependants’ Protection Scheme (DPS)

The Dependants’ Protection Scheme (DPS) is a term insurance that provides insured members and their families with some money to get through the first few years should the insured members pass away, suffer from Terminal Illness or Total Permanent Disability. This covers all Singaporeans and Permanent Residents (PR) who starts making CPF contributions. One advantage of the DPS is that the premiums are deducted from the CPF-OA and hence minimize the cash outlay for those cash-strapped to get some form of protection.

From 1 April 2021, changes will be made to Dependants’ Protection Scheme and it includes the following:

- Appoint Great Eastern Life as the sole insurer to administer Dependants’ Protection Scheme (DPS)

- Increase of sum assured from $46,000 to $70,000

- Increase of age coverage, to cover members up to age 65

| Age (Last Birthday) | Yearly Premium for $46,000 sum assured(before 1 April 2021) | Yearly Premium for $70,000 sum assured(From 1 April 2021^) |

| 34 years and below | $36 | $18 |

| 35 – 39 years | $48 | $30 |

| 40 – 44 years | $84 | $50 |

| 45 – 49 years | $144 | $93 |

| 50 – 54 years | $228 | $188 |

| 55 – 59 years | $260 | $298 |

| 60 – 64 years | Not applicable | $298 (for sum assured of $55,000) |

Premiums for most ages has been reduced, despite the higher coverage, with only those from 55-59 paying slightly more for the higher cover. What is good is that the cover has been extended to 65, more in line with the current retirement age. This will be better able to take care of the potential loss of a breadwinner in the family with more of us working till 65 or beyond.

MediShield Life

MediShield Life is a basic health insurance plan that helps to pay for large hospital bills and selected costly outpatient treatments such as dialysis and chemotherapy for cancer. It is basic because it is sized for subsidized treatment in public hospitals.

It provides lifetime coverage for all Singaporeans and PRs, even if they have pre-existing conditions.

The key recommended benefits include updating and refining the claim limits to provide better coverage, introducing treatment-specific claim limits for costlier types of community hospital care and outpatient radiotherapy, raising the policy year claim limit from $100,000 to $150,000, and allowing higher daily claim limits for the first two days of acute hospital stays, amongst others.

The higher daily claim limits for the first two days of acute hospital stays will provide better coverage for short stays for patients who can be discharged earlier. In support of this recommendation, the Government will also adjust the MediSave withdrawal limits for acute hospital stays in tandem, as shown in Table A. Taken together, the new MediShield Life and MediSave limits will result in lower out-of-pocket costs for patients.

Table A: New MediShield Life and MediSave daily ward and treatment limits for acute hospital stays*

| Day | MediShield Lifeclaim limit^ | MediSave withdrawal limit | Cumulative limit# |

| 1 | $1,000 ($700) | $550 ($450) | $1,550 ($1,150) |

| 2 | $1,000 ($700) | $550 ($450) | $3,100 ($2,300) |

| 3 and beyond | $800 ($700) per day | $400 ($450) per day | $4,300 ($3,450) in Day 3; additional $1,200 ($1,150) for each subsequent day |

^ This is the limit for normal ward stays. ICU ward stays are subject to a MediShield Life claim limit of $2,400 per day for the first two days and $2,200 per day from the third day onwards. The same MediSave withdrawal limit applies for both normal ward and ICU ward stays.

# Sum total of MediShield Life and MediSave limits, accumulated over the days.

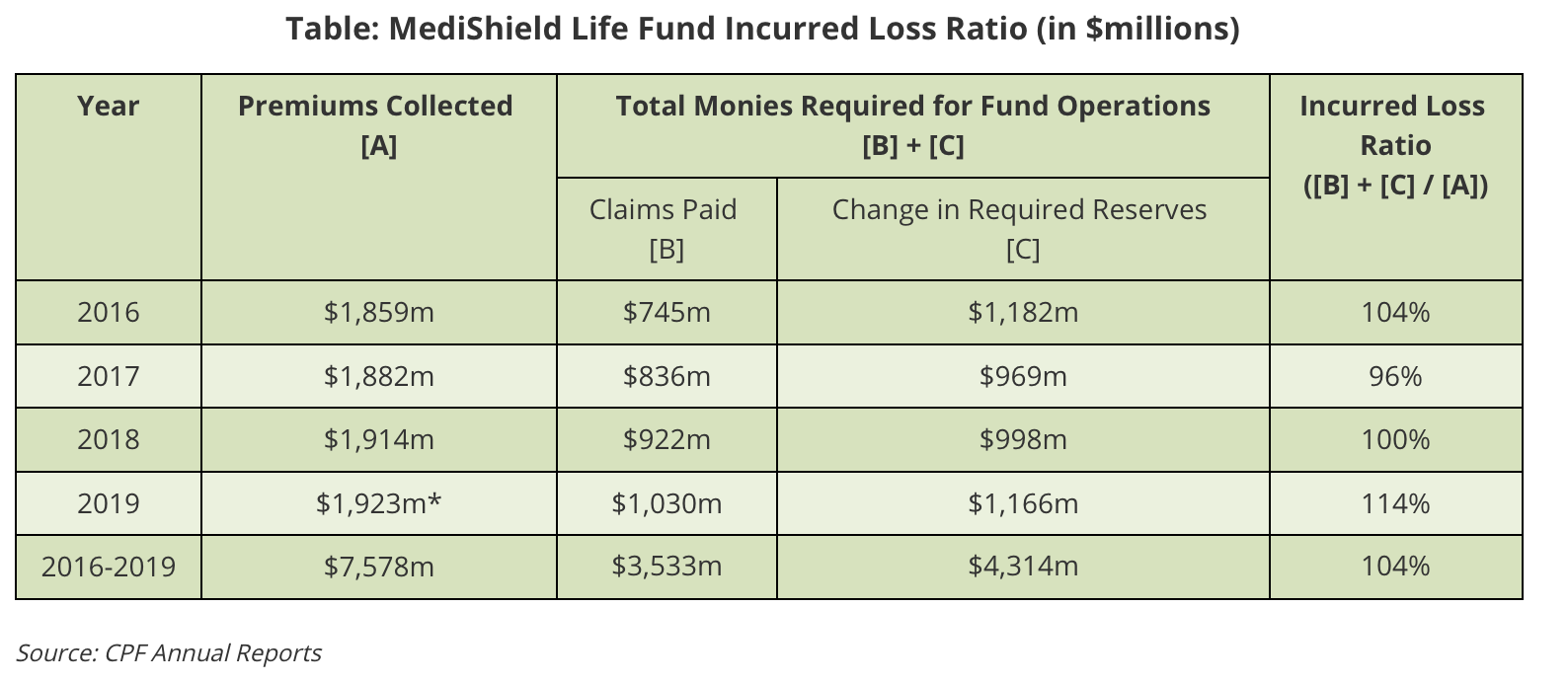

In tandem with the changes in coverage and to ensure the sustainability of the plan, premiums will also be increased. Even though the claims paid ratio currently is less than 50% of the premiums collected, the projected potential claims that could be incurred in the future, especially with an aging population, has increased the incurred loss ratio for the scheme, hence necessitating the increase in premiums.

To help Singaporeans cope with the increase in premiums, the government will provide up to $2.2 billion for premium subsidies and support over the next three years to help Singapore Residents with their premiums. This comprises $1.8 billion for existing premium subsidies and support measures for lower and middle-income households, PG and Merdeka Generation (MG) seniors, and the financially needy, and $360 million for the new COVID-19 Subsidy.

This will subsidize 70% of the net increase in premiums (after taking into account existing premium subsidies) in the first year, followed by 30% in the second year. Taken together with the existing premium support measures, the net premium increases for all Singapore Citizens will be kept to no more than about 10% in the first year.

Even with the enhancements in the scheme, it is important to know that Medishield Life is still a very basic hospital cover plan. For those of us who can afford to be more adequately covered and who require better healthcare options, it is still important to be covered appropriately with a suitable integrated private medical insurance. Unfortunately, premiums for private medical insurance, especially those that cover private hospitalization has shot up significantly over the years. Therefore, do speak with your financial adviser representative to understand your needs better so that a customized solution can be designed to suit your needs and save on unnecessary expenses.

CareShield Life

CareShield Life is a long-term care insurance scheme that provides basic financial support should Singaporeans become severely disabled, especially during old age, and need personal and medical care for a prolonged duration (i.e. long-term care). It replaces the previous ElderShield plan with a few key differences:

Lifetime coverage

You continue to be covered for life once you have completed paying all your premiums, which will happen in the year you turn age 67 or 10 years after you join the scheme, whichever is later.

Lifetime cash payouts

You will receive monthly payouts for as long as you remain severely disabled.

Payouts are in cash so that you and your caregiver have the flexibility to decide on your desired care arrangements (e.g. home care or nursing home care)

Payouts

Payouts start at $600/month in 2020 and increase over time

Your payouts will increase annually until age 67 or when a successful claim is made, whichever earlier. Once a successful new claim is made, your monthly payout amount will remain fixed for the duration of your severe disability.

From 2020 to 2025, payouts will increase by 2% per year. Thereafter, payout increases and corresponding premium adjustments will be recommended by an independent CareShield Life Council.

CareShield life was successfully rolled out to Singaporeans and PRs born from 1980 -1990 on 1 Oct 2020. It is a compulsory plan and for those born after 1991, you will be automatically enrolled into the plan as you turn 30.

It will be extended to those born in 1979 and before, in the second half of the year. To make joining more convenient, if you are born between 1970 and 1979 (aged 41 to 50 in 2020), insured under ElderShield 400, and not severely disabled, you will be automatically enrolled into CareShield Life from end-2021. However, you can opt-out by 31st Dec 2023 if you do not wish to remain on CareShield Life. If you are born before 1970, You can apply to join CareShield Life from the end-2021 onwards, if you are not severely disabled. There is no age limit to the cover and as long as you are not severely disabled (defined as already being unable to perform 3 out of 6 activities of daily living), you can be covered under the plan.

You will be sent the personalized premiums to enroll into CareShield Life when it kicks in later this year. The CareShield Life premiums are fully funded from the CPF Medisave account. The premium amount depends on a few factors, such as age, gender, whether you are already enrolled under ElderShield 300/400…etc. It consists of a base premium and a catch-up component for those who are not yet under the ElderShield 400 plan.

To encourage participation, there will be participation incentives given to those who join CareShield Life before 31 Dec 2023 and for Pioneer and Merdeka Generation seniors, the incentives could be up to $4,000 over 10 years. Besides, there will be further means-tested subsidies as well as additional premium support for those who are still unable to afford the premiums.

To opt-in or not to opt-in, that is the question

In the past, I have come across many clients who opted out of ElderShield when it was first introduced. Their rationale was that the payout is too low ($300/mth x 5 years = $18,000 only!) and too tough (to be unable to perform 3/6 ADLs seem too difficult).

While sharing CareShield Life with over 50 clients towards the end of last year, I have heard of numerous personal anecdotes from clients who shared that their loved ones have been unable to perform at least 3/6 ADLs for a prolonged period. One client’s granny was in a nursing home for almost 19 years!

In addition, I also have spoken to clients who are assessors for ADLs in the hospitals. With an aging population, there is an increasing pool of seniors who are unable to take good care of themselves and require help with their ADLs. They shared that the basis for these assessments of the ability to perform ADLs does not lie in the complete inability to perform the ADL, but in whether the ADLs can be performed “independently“. This means that those with cognitive impairment such as dementia, where they might not be in full control of their bladder, could also be able to qualify as one inability to perform the toileting ADL.

With CareShield Life now being a universal plan with a lifetime payout, where the underwriting requirements are less stringent, it, therefore, makes sense for those with already some form of health impairment to opt into the base plan. There are no loading or exclusion and even cancer or heart attack survivors who are otherwise unable to get proper insurance being able to enroll themselves into the plan. The government’s desire to be inclusive to take care of citizens and PRs make this an essential plan, especially given the sobering statistics from MOH.

- By 2030, 1 in 4 Singaporeans will be aged 65 or older

- 1 in 2 healthy Singapore residents aged 65 today could become severely disabled in their lifetime

- Half stay in disability for 4 years or more and 30% for 10 years or more.

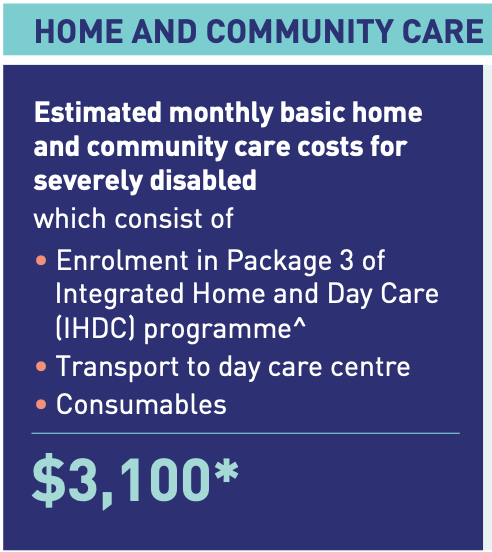

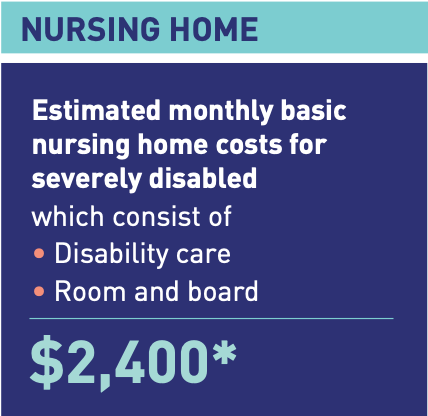

- The current cost of the nursing home or home and community care ranges from $2,400 to $3,100 a month.

In fact, for those of us who can afford to customize our cover better, we should enhance our coverage more comprehensively with a private long term care plan. MOH allows us to use our Medisave savings to fund our private long term care plan using $600/year from our Medisave savings with the rest of the top-up in cash. If affordability is not an issue, we should provide for 2/6 ADLs to ensure that if we are partially disabled, we would at least have some form of payout to offset our long term care cost.

One occupational therapist I spoke to shared that they err on the side of compassion in assessing ADLs and even then, many seniors are only borderline unable to perform 2/6 ADLs. With a comprehensive plan that can cover even just 2/6 ADLs, these seniors with some partial disability would be able to enjoy payouts to reduce the burden of care on the family.

Do speak to your financial adviser representative to discuss your long-term care financing to see how it can be optimized and help us live our life with ease and dignity should we be unfortunately stuck with some form of disability.

Sources: https://www.moh.gov.sg/home/our-healthcare-system/medishield-life/what-is-medishield-life/about-the-medishield-life-fund https://www.careshieldlife.gov.sg/content/dam/cshl/pdf/eldershield-review-committee-report.pdf

APEX Private Wealth Management (A group of advisers representing PIAS)

Alan Tang

Senior Financial Services Director

Mobile: 9679 9129

E-mail: alan.tang@proinvest.com.sg